An expense-reimbursement fraud investigation proves that an employee obtained money for expenses that were duplicated, mischaracterized, inflated, or fabricated—and it does so with data, documents, and a defensible chain of custody. The disciplined sequence is: preserve the reports and source records, run data tests to isolate the pattern, corroborate each suspect claim against original evidence, interview the employee last, then pursue discipline and recovery. Built correctly, the file supports restitution, insurance claims, and prosecution.

Why Expense-Reimbursement Fraud Is So Common and So Underestimated

Expense-reimbursement schemes are among the most frequent forms of occupational fraud precisely because they hide inside a legitimate, routine process. Every organization reimburses travel, meals, mileage, supplies, and client entertainment; approvers are busy, amounts are individually small, and the paper looks ordinary. The Association of Certified Fraud Examiners consistently reports that occupational fraud runs for roughly a year or more before detection, and that expense-reimbursement schemes are a leading category by frequency. The losses are rarely dramatic in any single transaction—they accumulate, month over month, under an approval that has become a rubber stamp.

What makes these matters dangerous for the employer is not the size of a single claim; it is the pattern. A padded mileage log or a personal dinner recoded as a client meeting is trivial in isolation, but a disciplined data review usually reveals a sustained habit stretching back years. That habit is what converts a minor HR annoyance into a provable financial-fraud case—and, because reimbursements often touch tax treatment under an accountable plan, into a matter with compliance exposure as well. The employer’s advantage is that the fraud lives in records the company already owns: expense reports, corporate-card feeds, receipts, calendars, and travel bookings.

What Are the Four Ways Expense Claims Are Faked?

Practitioners classify reimbursement fraud into four mechanisms. Correctly identifying which one you are dealing with determines which source records matter and which data tests will surface the proof.

| Scheme | What the employee does | Where it is proven |

|---|---|---|

| Duplicate | Submits the same expense more than once—on two reports, on both a report and the corporate card, or as a paper receipt and a scanned copy | Cross-matching reports to card feeds; detecting reused receipt images and identical amounts, dates, and vendors |

| Mischaracterized | Claims a genuine expense that was personal or non-reimbursable—a family dinner logged as client entertainment, a personal trip billed as business | Calendars, guest lists, itineraries, and business-purpose documentation that contradict the stated purpose |

| Inflated (overstated) | Submits a real expense but for more than was actually paid—altered receipts, padded tips, inflated mileage, or a higher currency conversion | Original vendor records, card settlement amounts, and point-to-point mileage recalculation |

| Fabricated (fictitious) | Invents an expense that never occurred—a forged or template receipt, a claim for a canceled trip, a phantom vendor | Vendor confirmation, receipt-authenticity forensics, and the absence of any corroborating card or travel record |

A single employee often blends several mechanisms—duplicating a legitimate hotel folio one month, mischaracterizing a personal meal the next, and rounding up mileage throughout. Treating the matter as one undifferentiated “expense problem” wastes the investigation’s leverage. Each mechanism has its own signature and its own test.

The Seven-Phase Expense-Fraud Investigation Framework

Elite financial investigations follow a deliberate order. Acting out of sequence—confronting the employee before the data is analyzed, or letting an approver “look into it” informally—is the fastest way to turn a strong case into an unprovable one and to hand the employee a retaliation claim.

- Predication and scoping. Document what prompted the concern—a tip, an anomaly, a duplicated charge—and confirm a reasonable, articulable basis before anyone is investigated. Restrict knowledge to the smallest circle: ownership or general counsel plus the lead investigator. Do not alert the suspect’s manager or the approver until you know they are not involved.

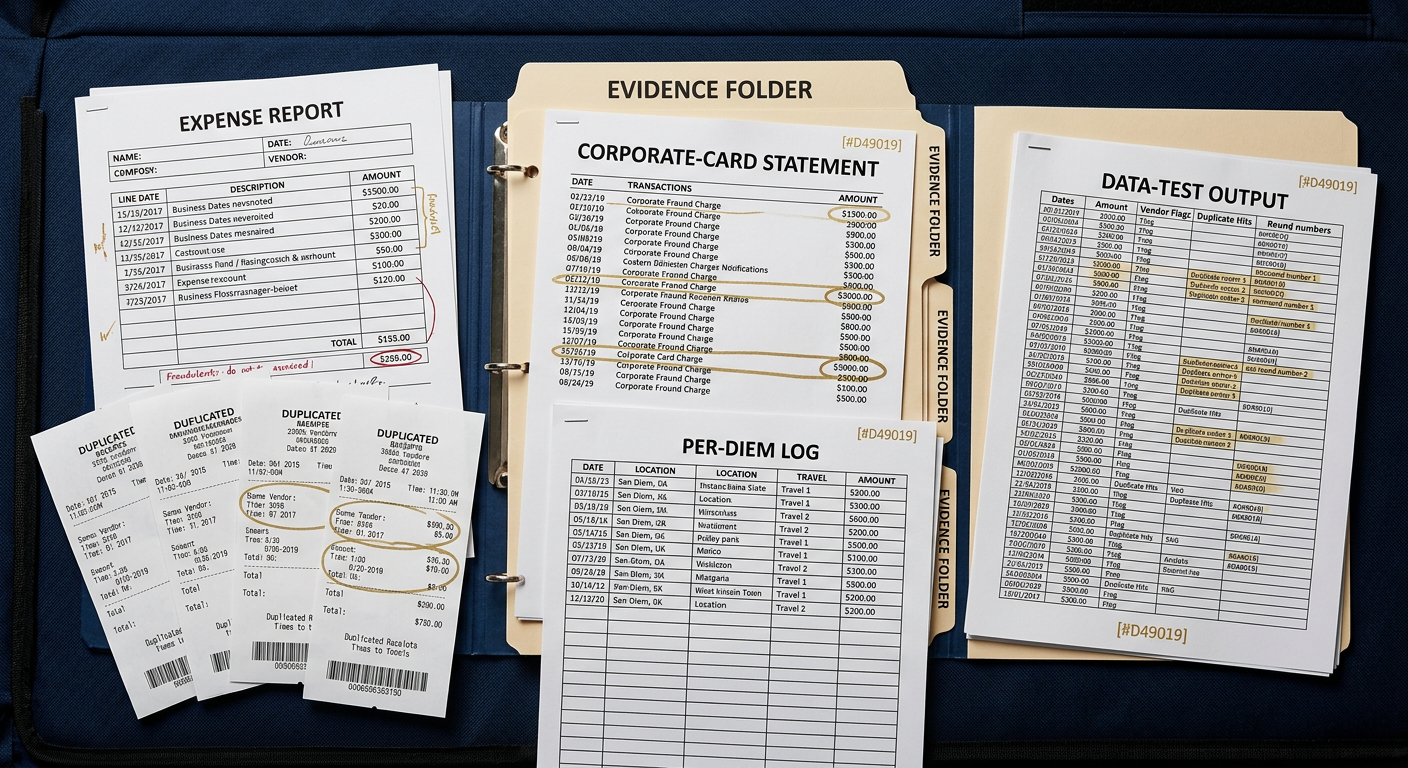

- Silent evidence preservation. Secure the records the employee could alter or delete: submitted expense reports and attachments, corporate-card transaction feeds, the accounts-payable file, email, calendar, travel-booking records, and any expense-system audit log. Preserve them as originals—exports with metadata intact—not screenshots.

- Data testing. Run the analytical tests below across the full population, not a sample, to isolate outliers by employee, category, vendor, and time. The goal is a ranked list of suspect claims tied to a person and a mechanism.

- Document-level corroboration. Pull the original source for each flagged claim—the vendor folio, the card settlement, the calendar entry—and prove the discrepancy item by item. This is where a suspicion becomes a quantified loss.

- Receipt and record forensics. Examine questioned receipts for signs of alteration or fabrication (edited images, inconsistent fonts, reused templates, impossible sequence numbers) and confirm authenticity directly with vendors where warranted.

- The interview—last, never first. With the record built, a trained investigator conducts a voluntary, non-accusatory interview to obtain a truthful account and, where warranted, a signed statement. Facts established beforehand let the interviewer test the account rather than beg for a confession.

- Discipline, recovery, and control remediation. Findings drive proportionate action—termination, restitution, civil recovery, a fidelity-bond or insurance claim, tax correction where required, and a criminal referral where appropriate—plus the control fixes that close the gap the scheme exploited.

Which Data Tests Actually Expose the Fraud?

Data analytics is the quietest and most powerful tool available, because it never tips the suspect and it scales to years of history in minutes. Modern expense platforms and card feeds hold far more structure than most reviewers examine. The art is exception-based testing—filtering the entire transaction population down to the statistically abnormal, then attributing each anomaly to an employee, a category, and a date.

- Duplicate detection: match on amount, date, vendor, and near-identical receipt images across reports, and cross-match every report line against the corporate-card feed to catch the classic “claimed it and charged it” double dip.

- Round-number and just-under-threshold analysis: clusters of even amounts ($50.00, $100.00) suggest estimates rather than real receipts, and charges consistently landing just below a receipt-required or approval threshold (for example $24.99 where $25 triggers scrutiny) indicate deliberate structuring.

- Benford’s Law and digit analysis: genuine expense populations follow a predictable distribution of leading digits; a claimant whose figures deviate—too many amounts beginning with certain digits—flags fabricated or inflated numbers for closer review.

- Weekend, holiday, and out-of-pattern spend: business expenses on days the employee was not traveling, or in cities where they had no meetings, expose mischaracterized personal spending.

- Per-diem and mileage recalculation: compare claimed mileage against point-to-point routing and claimed per diems against published rates (the U.S. General Services Administration sets federal rates many firms mirror); systematically padded distances and rates surface immediately.

- Vendor and sequence anomalies: a personal vendor appearing only on one employee’s reports, or receipt/invoice numbers that fall out of chronological sequence, point to fictitious claims.

- Velocity and threshold-timing: spikes right before period close, or submissions timed to a lenient approver’s shift, reveal an employee working the process rather than incurring costs.

The decisive move is correlation: overlay the exceptions with calendars, travel bookings, badge or location data, and card settlements until a single employee sits at the center of the pattern. When the tests and the source documents agree, you no longer have a suspicion—you have a quantified case. This is precisely where in-house financial investigation and digital forensics earn their keep, because reconstructing altered receipts and recovering deleted expense-system records requires forensic tooling, not a spreadsheet.

How Do You Prove Each Dollar and Build a Defensible File?

A data flag is a lead, not proof. Prosecutors, arbitrators, and civil courts want each claimed dollar tied to a specific document that contradicts it. That means reconstructing every flagged transaction to its original source and quantifying the loss item by item.

- Duplicate claims: place the two submissions side by side—the report line and the card charge, or the two reports—and show the identical amount, date, and vendor, with the receipt reused on both.

- Mischaracterized claims: pair the claim’s stated business purpose against the contradicting record—a calendar showing no meeting, a guest list of family members, an itinerary that was a personal vacation.

- Inflated claims: obtain the vendor’s original folio or the card-settlement amount and demonstrate the delta between what was paid and what was claimed; for mileage, attach the routing recalculation.

- Fabricated claims: document the absence of any supporting card or travel record and, where possible, obtain written confirmation from the vendor that no such transaction occurred—or a forensic finding that the receipt was edited or template-generated.

Chain of custody is the pivot that makes the file survive challenge. Every artifact—an exported expense report, a card statement, a forensic image of the laptop where a receipt was doctored, a signed statement—must be collected soundly, logged, stored securely, and traceable from acquisition to production. Digital evidence is fragile: opening a receipt image can change its metadata, and a screenshot of an expense system is not the same as a metadata-intact export from that system. Assume every step will be read aloud in a deposition; if a shortcut would look sloppy to a judge, it is not worth the marginal speed.

What Are the Legal and Tax Dimensions Owners Miss?

Reimbursement fraud is not only a workplace-discipline issue; it carries legal and tax consequences that shape how the investigation should be run. First, reimbursements paid under an accountable plan are tax-free to the employee only when they are substantiated business expenses returned within a reasonable period; amounts that turn out to be personal, unsubstantiated, or fabricated can lose that treatment and become taxable wages, creating payroll-tax and reporting corrections. The Internal Revenue Service sets the substantiation standard, so a fraud finding can trigger a compliance clean-up as well as a recovery.

Second, the investigation itself must respect the same employee-protection lines that govern any internal inquiry. Do not conduct a coercive interview, block exits, or confiscate a phone—those create false-imprisonment exposure regardless of guilt. Do not announce “the thief” to staff before findings, which invites a defamation claim. Watch the timing of any adverse action against protected activity (a wage complaint, a leave request, a discrimination report) to avoid a retaliation claim. And in a public-sector employer, compelled statements can carry Garrity protections that bar criminal use—a scenario where counsel must shape the interview in advance. Structuring the matter with these constraints designed in, rather than patched after a complaint, is what separates a professional investigation from a lawsuit waiting to happen.

How Do You Recover the Money and Deter the Next Scheme?

Most organizations want three outcomes: stop the bleeding, recover the loss, and make an example that deters repetition. Each depends on the quality of the file. Recovery runs on several parallel tracks, and the strongest cases pursue more than one.

- Restitution and repayment. A quantified, document-backed loss supports a demand for repayment—often through a negotiated agreement or as a condition of separation—and, where a matter is charged, as court-ordered restitution.

- Fidelity or employee-dishonesty bond. Many firms carry crime coverage that reimburses proven employee theft; carriers require a properly documented loss and often a cooperation obligation, so the case file must meet their evidentiary bar.

- Civil recovery. Where amounts justify it, civil claims for conversion, breach of fiduciary duty, or fraud can reach assets beyond the employee’s paycheck.

- Criminal referral. Prosecutors take cases packaged to charge: a clear scheme narrative, the loss quantified and tied to specific dates and dollars, the data tests and source documents, an intact chain of custody, and any voluntary statement. Vague totals and missing custody records get declined.

- Tax and reporting correction. Where fabricated or personal amounts lose accountable-plan treatment, correct the payroll and reporting exposure so the fraud does not metastasize into a compliance problem.

Deterrence, finally, is a controls exercise as much as a disciplinary one. The single best signal a company can send is that expenses are actually reviewed—analytically, not ceremonially.

Which Controls Prevent Reimbursement Fraud Going Forward?

A completed investigation should always close with control remediation, because the scheme succeeded through a specific gap. Effective, proportionate controls include:

- Independent review, not self-approval. No one approves their own expenses, and executives—whose reports are the least scrutinized and the highest-value—are reviewed by someone with real authority to question them.

- Original, itemized receipts with business purpose. Require itemized documentation and a stated business purpose above a low threshold, and disallow the round-number estimate.

- Continuous data monitoring. Run the duplicate, round-number, weekend, and per-diem tests on a scheduled basis rather than waiting for a tip; automated exception reporting turns detection from luck into routine.

- Corporate-card reconciliation. Match card feeds against expense claims automatically so a duplicate double-dip is caught at submission, not years later.

- Clear, written policy and consequences. A specific reimbursement policy—what is reimbursable, what documentation is required, and that violations lead to discipline and recovery—removes the “I didn’t know” defense and raises the perceived cost of trying.

- Periodic independent audit. A rotating, unannounced review of a sample of reports signals that any claim might be examined, which is itself a powerful deterrent.

These controls do not require a large department—they require design and follow-through. For organizations without in-house forensic-accounting capacity, standing up the monitoring and running the periodic review through an external firm is often more cost-effective and more credible than building it internally.

What Separates a World-Class Expense-Fraud Investigation From a Mediocre One?

Every firm claims to “look into” expenses. The difference shows when the case is challenged, the employee retains counsel, or a carrier demands proof.

- Full-population data testing, not sampling. Amateurs eyeball a few reports; professionals test every transaction across years and rank the outliers objectively.

- Every dollar tied to a document. The case rests on source records that contradict each claim—card settlements, vendor folios, calendars—not on how someone “seems.”

- Legal and tax boundaries engineered in. Privacy, false-imprisonment, retaliation, and accountable-plan rules are part of the plan from hour one.

- Forensic capability in-house. Digital forensics, financial investigation, cybersecurity, and background intelligence under one command mean altered receipts and deleted records are recoverable, not lost. Honeybadger Solutions runs these functions in-house and remote-by-design, nationwide and internationally.

- A file built for recovery and court. Chain of custody, a quantified loss, and an un-coerced statement make the package collectible on a bond, chargeable by a prosecutor, and durable in arbitration—the true measure of a completed investigation.

National Reach, Discreet Command

Honeybadger Solutions supports employers across Arizona, nationwide, and internationally. Because reimbursement fraud lives in records—expense systems, card feeds, email, and cloud storage—our digital forensics, cybersecurity, financial investigations, and background intelligence functions are global and remote-by-design, so an inquiry can be stood up quickly and quietly wherever the employee and the data sit. Field investigation and protective operations are commanded through a vetted-partner network, with Arizona as home command and established theaters in California, Texas, and Florida. Whether the matter is a single padded travel report or a multi-year, multi-mechanism scheme by a senior executive, the process and the standard are the same.

Frequently Asked Questions

How far back should an expense-fraud investigation look? As far as the records reasonably allow, because these schemes are habitual and the recoverable loss usually grows the further back you test. Most expense platforms and card feeds retain several years of history. A full-population data review across all available periods both maximizes recovery and demonstrates the sustained pattern that makes a matter prosecutable, rather than dismissible as a one-time mistake.

Can padded mileage or a mischaracterized dinner really be a crime? Individually the amounts are small, but a sustained pattern of knowingly false claims can constitute theft, fraud, or embezzlement depending on the jurisdiction and the total. The decisive factors are intent and repetition: an isolated honest error is not fraud, but a documented, recurring practice of overstating or inventing expenses is. Prosecutors and courts look at the aggregate scheme, not a single line.

Should we confront the employee as soon as we spot a duplicate charge? No. Confronting on the first flag warns the employee to alter or delete records, stops the provable behavior, and exposes the company to retaliation and defamation claims. Preserve the reports and source data, run the full data analysis, corroborate each claim against original documents, and interview last—in that order. A confrontation before the file is built almost always weakens the case.

Will our insurance cover the loss? Many firms carry a fidelity or employee-dishonesty bond that reimburses proven employee theft, including reimbursement fraud, but carriers require a properly documented, quantified loss and often timely notice and cooperation. That is another reason to build the file to an evidentiary standard from the outset: the same documentation that supports prosecution and restitution is what the carrier will demand before it pays.

About Honeybadger Solutions

Honeybadger Solutions is an Arizona-licensed security and investigations firm serving all of Arizona, the nation, and international clients. We combine in-house digital forensics, cybersecurity, financial investigations, and background intelligence with a vetted network for field and protective operations. Our teams build discreet, legally defensible expense-fraud cases designed to survive litigation, satisfy carriers, and support prosecution and recovery.

Three offices: Casa Grande (HQ), Phoenix, and Oro Valley. To discuss a confidential matter, call 602-725-2818. Learn more about our corporate and internal investigations capabilities, our approach to financial investigations, and our digital forensics practice, or reach our Phoenix team to request a discreet consultation.