Procurement fraud is the manipulation of the buying process itself—not the vendor relationship alone—to divert money or steer business improperly. The classic red flags are split purchase orders that dodge approval thresholds, sole-source awards that avoid competition, and undisclosed conflicts of interest between buyers and suppliers. It is surfaced through buying-pattern analytics on the organization’s own spend data and confirmed through a disciplined, evidence-first investigation.

Most fraud coverage treats “vendor fraud” as a single problem—a bad supplier overbilling a trusting customer. Procurement fraud is a different and more corrosive animal. Here the weakness is inside the buying process, and the person exploiting it usually holds legitimate authority: a buyer, a budget owner, a contracting officer, or an approver who understands exactly where the controls have gaps. Because the transactions look ordinary and the perpetrator is trusted, procurement fraud is among the longest-running and most expensive schemes an organization faces. This is the operational guide to the red flags that expose it and the investigative method that proves it.

What Counts as Procurement Fraud—and How Is It Different From Vendor Fraud?

Procurement fraud is any scheme that corrupts the process of acquiring goods or services—sourcing, bidding, award, purchase order, receipt, and payment—to produce an improper benefit. Vendor fraud, by contrast, is what an external supplier does to a customer: overbilling, duplicate invoicing, or delivering less than promised. The two overlap, but the distinction matters operationally, because procurement fraud almost always requires an insider, or an insider-supplier collusion, and that changes both the red flags and the investigative approach.

The Association of Certified Fraud Examiners classifies these schemes under corruption—conflicts of interest, bid-rigging, kickbacks, and illegal gratuities—and its Report to the Nations consistently identifies corruption as one of the most common occupational fraud categories and among the costliest to detect, because collusion defeats the segregation-of-duties controls that catch simpler theft. Procurement is where corruption most often lives, because it sits at the intersection of authority, money, and outside relationships. The schemes below are the ones a professional investigator expects to find.

| Scheme | How it works | Primary red flags | Where it shows in the data |

|---|---|---|---|

| Split purchase orders | A single purchase is broken into smaller POs to stay under an approval or competitive-bid threshold | Multiple orders to one vendor just below a limit, close in time, for related items | Clusters of POs at 90–99% of an approval threshold, same vendor, same requester, same week |

| Sole-source / non-competitive abuse | Competition is bypassed with a weak or boilerplate “only qualified vendor” justification | Recurring sole-source awards, vague justifications, urgency manufactured to skip bidding | High share of non-competitive spend concentrated in one buyer or one vendor |

| Bid-rigging | Ostensibly competitive bids are coordinated so a predetermined vendor wins | Same losing bidders every time, near-identical bids, rotating winners, complementary high bids | Narrow, patterned bid spreads; the same runner-up appearing across tenders |

| Kickbacks & bribery | A vendor pays a buyer to win or keep business, funded by inflated prices | Prices above market, buyer resists changing vendors, lifestyle beyond salary | Rising unit costs vs. benchmarks; one vendor’s share climbing without a business reason |

| Conflict of interest | The buyer has an undisclosed financial or personal tie to the vendor | Shared addresses, family names, ex-employee vendors, no disclosure on file | Vendor master data matching employee records (address, phone, bank, tax ID) |

| Shell / phantom vendors | A fake vendor controlled by an insider is paid for goods or services never delivered | New vendor with a P.O. box, no web presence, invoices with sequential numbers only to you | Vendor set up shortly before first payment; round-dollar invoices; no receiving records |

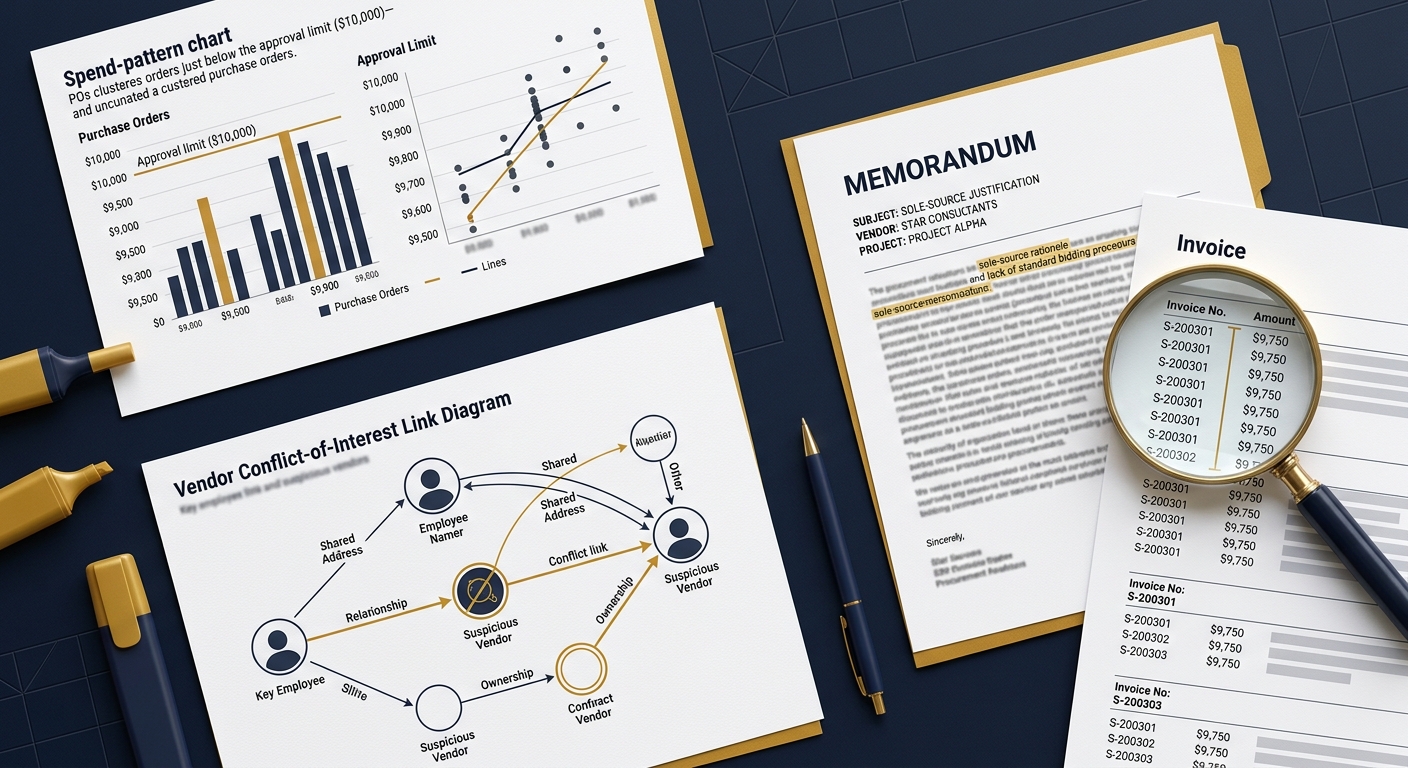

Why Are Split Purchase Orders the Most Common Red Flag?

Every procurement system runs on thresholds. Below a dollar limit a buyer can approve a purchase alone; above it, a second approval, a competitive quote, or a formal bid is required. Splitting is the deliberate fragmentation of one real requirement into two or more purchase orders, each engineered to fall just under that limit—so the higher scrutiny never triggers. It is the most common procurement red flag precisely because it requires no outside accomplice and exploits a control that everyone knows exists.

The signature is statistical, not anecdotal. In clean spend data, purchase amounts distribute naturally across a range. In a splitting environment, an unnatural cluster forms just beneath the threshold—many orders at, say, $9,400–$9,900 against a $10,000 approval limit, frequently to the same vendor, from the same requester, within a compressed window. Investigators test for this by plotting purchase-amount frequency around each control threshold and by grouping same-vendor, same-requester orders within short date ranges. A genuine business need occasionally produces two close orders; a pattern of them, hugging the line, is a scheme. The tell is not any single order but the shape of the distribution.

When Does Sole-Source Contracting Become Abuse?

Sole-source (non-competitive) awards are legitimate and sometimes unavoidable—a proprietary part, a single certified provider, a genuine emergency. Abuse begins when the justification is manufactured to avoid competition and steer the award to a favored vendor. The federal framework is instructive here: agencies must document a specific, defensible basis before bypassing competition, and the same logic transfers directly to corporate procurement. Where the justification is boilerplate, recycled across unrelated buys, or built on an “urgency” the buyer created by delaying, the control has failed.

The red flags cluster around three things: frequency (one buyer or one vendor accounts for a disproportionate share of non-competitive spend), justification quality (vague, templated, or unsupported “only qualified source” claims), and manufactured urgency (requirements that could have been competed are pushed through as emergencies to skip bidding). Investigators pull every sole-source justification for a period, score them for substance, and map them to the awarding buyer and receiving vendor. Concentration is the signal—abuse is rarely a single bad memo; it is a habit visible only when the awards are aggregated. Sole-source abuse also frequently masks the schemes beneath it: it is the mechanism through which kickbacks and bid-rigging are delivered, because eliminating competition is the whole point.

How Do Undisclosed Conflicts of Interest Hide in the Data?

A conflict of interest exists when the person influencing an award has an undisclosed personal or financial stake in the outcome—an ownership interest in the vendor, a family relationship, a side arrangement, or a former employer now selling back to the company. Conflicts are dangerous because they corrupt the decision quietly: the transactions themselves can look entirely normal while every one of them tilts toward a party the buyer is secretly aligned with.

The most productive detection technique is a structured cross-match between the vendor master file and employee records. Investigators compare addresses, phone numbers, email domains, bank account and routing numbers, and tax identification numbers across the two data sets. A vendor whose remittance address matches an employee’s home, whose bank account matches a payroll account, or whose principals share a surname and address with a buyer is a conflict until proven otherwise. This work extends into open-source and corporate-registry research—confirming beneficial ownership, prior employment, and related entities—which is where our corporate investigations and background-intelligence capabilities do the heavy lifting. Enforcing an annual, documented conflict-of-interest disclosure is the control; the data cross-match is how you catch what people fail to disclose.

Which Buying-Pattern Anomalies Signal Fraud?

Modern procurement investigation is data-led. Before anyone is interviewed, the analytics run against the organization’s purchasing, accounts-payable, and vendor-master data, because the money leaves a pattern that memory and paperwork cannot fully conceal. The recurring anomalies a forensic team tests for include:

- Threshold clustering. Purchase amounts bunching just below approval or bid limits—the fingerprint of splitting.

- Vendor concentration without cause. One vendor’s share of a category rising steadily, or a buyer routing a disproportionate volume to a single supplier absent a contract or price advantage.

- Off-benchmark pricing. Unit costs drifting above market or above other business units for the same item—the funding source for kickbacks.

- Duplicate and near-duplicate payments. The same invoice number, amount, or date paid more than once, or slight variations engineered to slip past a three-way match.

- Round-dollar and sequential invoices. Invoices in even amounts, or numbered sequentially only to your company—hallmarks of a phantom vendor with no other customers.

- New-vendor-to-first-payment velocity. A vendor created and paid within days, especially by the employee who set it up.

- Missing receiving records. Payments with no corresponding goods-received entry—services and “consulting” are the classic cover, because nothing physical arrives.

- Weekend, after-hours, or backdated entries. Vendor-master changes or approvals made outside normal patterns, or timestamps that do not match the claimed sequence.

None of these is proof on its own—each has an innocent explanation, and a competent investigator assumes so until the record says otherwise. Their power is cumulative. When threshold clustering, vendor concentration, off-benchmark pricing, and a conflict-of-interest match all point at the same buyer-vendor pair, the analytics have not just raised a flag; they have built the spine of the case the interviews will later test.

How Do You Investigate Procurement Fraud Without Tipping Off the Subject?

A procurement fraud investigation is quiet, evidence-first, and sequenced so the subject—who usually still controls the relevant systems—learns nothing until the record is secured. The following framework is the order an elite team executes.

- Establish privilege and a small circle. Engage under counsel so analysis and findings are protected, and restrict knowledge to a need-to-know group that excludes the subject and anyone who reports to them. Over-notification is how targets get tipped off.

- Preserve the data before anyone is alerted. Forensically capture the purchasing, accounts-payable, vendor-master, email, and approval-log data, and issue a litigation hold. Vendor-master and PO records are trivially editable; secure immutable copies first.

- Run the analytics. Test for threshold clustering, vendor concentration, pricing anomalies, duplicate payments, phantom-vendor markers, and vendor-to-employee cross-matches. Let the data nominate the suspect transactions and relationships.

- Reconstruct the paper and digital trail. For each flagged transaction, assemble the full lifecycle—requisition, justification, approvals, PO, receiving record, invoice, payment—and identify where documents are missing, altered, or out of sequence.

- Verify the vendor is real. Confirm existence, ownership, and legitimacy through corporate registries, tax records, physical-address checks, and exclusion databases such as the U.S. System for Award Management for debarred parties. A vendor that dissolves on inspection is often the whole case.

- Trace the money. Follow payments through to their destination—where funds ultimately land, and whether any flow back to an insider—work anchored by our financial investigation practice.

- Interview outward-in. Only after the record is built, interview peripheral witnesses first and the subject last, so the subject responds to specific, evidenced transactions rather than a fishing expedition.

- Report to the applicable standard. Document findings on a preponderance-of-the-evidence basis, tied to cited records, in the format counsel specifies and built to survive litigation, arbitration, insurance review, or referral to law enforcement.

The digital dimension is decisive throughout. Approval logs, email between buyer and vendor, edited spreadsheets, and vendor-master change histories all carry metadata that establishes who did what and when—evidence that must be captured to forensic standards to survive challenge, the province of our digital forensics team. Screenshots taken by a nervous manager do not survive a courtroom; a properly acquired, hashed, and logged image does.

Which Controls Actually Prevent Procurement Fraud?

Detection catches fraud after the money has moved; controls stop it from moving. The U.S. Government Accountability Office’s Fraud Risk Management Framework makes the point that leading organizations manage fraud risk proactively—assessing exposure, designing controls to the specific schemes, and monitoring continuously—rather than reacting to losses. Applied to procurement, the highest-value controls are:

- Enforced segregation of duties. No single person requests, approves, receives, and pays. Splitting these roles is what forces collusion—and collusion is harder and riskier than solo theft.

- Threshold and splitting surveillance. Automated alerts for orders clustering below approval limits and for same-vendor, same-requester orders within short windows. This directly neutralizes the most common scheme.

- Sole-source justification discipline. Require substantive, reviewed justifications for every non-competitive award, and periodically audit the concentration of non-competitive spend by buyer and vendor.

- Vendor-master governance. Independent verification before onboarding, periodic re-validation, cross-matching against employee data, and tight control over who can create or edit vendor records—with every change logged.

- Mandatory conflict-of-interest disclosure. Annual, documented disclosures from everyone with buying authority, reconciled against vendor data rather than trusted at face value.

- Three-way match and continuous monitoring. PO, receiving record, and invoice must reconcile before payment, backed by ongoing analytics rather than an annual audit that samples a sliver of transactions.

- A protected reporting channel. Tips remain the single largest source of fraud detection; an anonymous, credible hotline routinely outperforms every automated control combined.

The strategic point is that controls and analytics are the same discipline viewed from two directions. The anomaly you monitor for in an investigation is the alert you should have been running all along. A mature program closes that loop—every scheme uncovered becomes a permanent detection rule—so the organization is not merely cleaning up one fraud but hardening the process against the next.

National Reach, Discreet Command

Honeybadger Solutions investigates procurement and corruption schemes for clients across Arizona, nationwide, and internationally. Our digital forensics, cybersecurity, financial investigations, and background-intelligence functions are in-house and remote-by-design, so data preservation and spend analytics can begin within hours of engagement no matter where the purchasing organization operates. Field and protective operations are commanded through a vetted-partner network, with Arizona as home command and established theaters in California, Texas, and Florida. Whether the exposure is a single suspect buyer or an enterprise-wide vendor scheme, the method and the standard do not change—explore our full corporate investigations and security capabilities, or reach our teams through the Phoenix office.

Frequently Asked Questions

What is the difference between procurement fraud and vendor fraud? Procurement fraud corrupts the buying process from the inside—split purchase orders, rigged bids, steered sole-source awards, and conflicts of interest—and almost always requires an insider or insider-supplier collusion. Vendor fraud is what an external supplier does to a customer, such as overbilling or duplicate invoicing. Procurement fraud is harder to detect because the perpetrator holds legitimate authority and the transactions look normal.

What are the most common red flags of procurement fraud? Purchase orders clustering just below approval thresholds (splitting), a high or rising share of non-competitive sole-source awards, vendor concentration without a business reason, prices above market benchmarks, duplicate or round-dollar invoices, new vendors paid within days of creation, missing receiving records, and vendor details that match an employee’s address, bank account, or tax ID.

How is data analytics used to detect procurement fraud? Investigators run tests against purchasing, accounts-payable, and vendor-master data to surface patterns—threshold clustering, vendor concentration, pricing anomalies, duplicate payments, phantom-vendor markers, and vendor-to-employee cross-matches. The analytics nominate the suspect transactions and relationships before anyone is interviewed, so the case is built on objective records rather than memory, and the subject is not tipped off.

How do you investigate procurement fraud without alerting the suspect? Engage under counsel, restrict knowledge to a small need-to-know circle that excludes the subject, and forensically preserve the relevant data and email before anyone is alerted—because vendor and purchase-order records are easily edited. Analytics and trail reconstruction come next, vendors and money are traced, and only then are interviews conducted outward-in, with the subject last.

About Honeybadger Solutions

Honeybadger Solutions is an Arizona-licensed security and investigations firm serving all of Arizona, the nation, and international clients. We combine in-house digital forensics, cybersecurity, financial investigations, and background intelligence with a vetted network for field and protective operations. Our teams uncover procurement and corruption schemes discreetly and build findings that withstand litigation, arbitration, insurance review, and law-enforcement referral.

Three offices: Casa Grande (HQ), Phoenix, and Oro Valley. To discuss a confidential matter, call 602-725-2818. Learn more about our corporate and internal investigations capabilities and request a discreet consultation.