Mortgage and real estate fraud investigation is the forensic and financial examination of a property transaction to determine whether it was procured through deception — a fabricated borrower, an inflated appraisal, a forged deed, a diverted closing wire, or a misrepresented occupancy or income — and to build attributable, court-ready proof of who did it and how. Done at an elite level it reconstructs the money trail, authenticates the documents, resolves the true parties behind the loan, and delivers findings a lender, title insurer, or litigator can act on.

Real estate is the largest asset most people ever touch and the largest single transaction most institutions underwrite in a day. That scale, combined with tight closing timelines, digital document flow, and multiple parties who never meet in person, makes it one of the most attractive targets for fraud in the modern economy. The schemes range from a single borrower shading the truth on an application to organized rings that manufacture entire transactions from stolen identities and complicit insiders. This guide is written for the lender, title and escrow executive, general counsel, family office, and private principal who must decide whether a deal is clean, unwind one that is not, and pursue recovery when money has already moved. It explains how the principal schemes actually work, how each is detected and proven, and what separates a defensible investigation from a checklist.

What counts as mortgage and real estate fraud?

Mortgage and real estate fraud is any material misstatement, misrepresentation, or omission — or any outright forgery or theft — made in connection with a property transaction or loan, relied upon by a lender, insurer, buyer, or seller to their detriment. Investigators and prosecutors draw a broad line between two motives. Fraud for housing is committed by borrowers who want a home they cannot legitimately qualify for and shade income, assets, employment, or occupancy to get the loan. Fraud for profit is committed by industry insiders and organized actors — loan officers, appraisers, closing agents, straw-buyer recruiters — who exploit the transaction itself to extract money, with the property merely the vehicle.

The distinction matters because it drives the investigation. Fraud-for-housing cases usually center on one loan file and a handful of documents. Fraud-for-profit cases are conspiracies: the same appraiser, the same closing agent, the same LLC, or the same recruiter recurs across many files, and the real work is pattern detection across transactions rather than scrutiny of a single one. The U.S. Federal Bureau of Investigation classifies mortgage fraud as a form of white-collar crime and monitors it as a persistent threat to the financial system; its mortgage fraud program exists precisely because the losses are large, the schemes are repeatable, and the same actors resurface.

What are the most common schemes?

Most real estate fraud reduces to a handful of recurring mechanisms. Understanding how each one is constructed is the prerequisite to detecting it, because every scheme leaves a characteristic signature in the documents, the money movement, or the parties. The table below maps the principal schemes to how they work and the evidence that exposes them.

| Scheme | How it works | Primary evidence trail |

|---|---|---|

| Straw buyer | A qualified or fabricated identity fronts a loan for a hidden true beneficiary who cannot or will not qualify | Identity mismatch, no occupancy, funds and payments from a third party, quick title transfer |

| Appraisal fraud | Property value is inflated (or deflated in a flip) to justify an oversized loan or a below-market acquisition | Comparable-sales manipulation, appraiser conflicts, valuation outliers, coordinated flips |

| Title and deed fraud | A forged deed or stolen identity transfers or encumbers property the fraudster does not own | Forged signatures and notarizations, chain-of-title breaks, absentee-owner targeting |

| Closing wire fraud | Compromised email diverts the buyer’s or lender’s closing funds to a fraudulent account | Spoofed domains, altered wire instructions, mule accounts, email-header forensics |

| Occupancy / income misrep | Borrower falsely claims owner-occupancy or overstates income and assets to qualify | Address and utility records, employment verification, bank-statement and tax analysis |

| Illegal property flipping | Rapid resale between colluding parties at fraudulently inflated prices | Short hold periods, price jumps, related-party transfers, straw participants |

These schemes rarely appear in isolation. A single fraud-for-profit conspiracy commonly combines a straw buyer, an inflated appraisal, and a complicit closing agent in one transaction — which is why a competent investigation examines the whole file and the whole network, not one alleged act.

How do straw-buyer schemes actually work?

A straw buyer is a person whose name and credit are used to obtain a mortgage for the real beneficiary of the transaction, who stays off the paperwork. The straw may be a willing participant paid a fee, an unwitting victim whose identity was stolen, or a relative pressured into lending their credit. The tell is almost always a divergence between the person on the loan and the economics of the deal: the down payment and monthly payments originate from someone else, the borrower never occupies or even visits the property, and title or control shifts to the hidden principal shortly after closing.

Proving a straw-buyer scheme is an exercise in connecting identity to money to control. Investigators verify the borrower’s genuine financial capacity against the funds that actually moved, trace the source of the down payment and the servicing payments, and establish whether the nominal owner exercised any real dominion over the property. Where the straw is a stolen identity, the work extends into digital forensics and background intelligence to prove the named borrower never applied at all. The pattern signature is decisive in fraud-for-profit rings: the same recruiter, the same funding source, or the same eventual beneficiary recurring across multiple straw transactions turns a series of individually plausible loans into a demonstrable conspiracy.

How is appraisal and valuation fraud detected?

Appraisal fraud manipulates the single number the entire loan depends on. Inflated valuations let a fraudster borrow far more than a property is worth — the difference is stripped out at closing and the loan is left to default against inadequate collateral. In a flip, coordinated appraisals inflate a resale price between colluding parties. The manipulation is achieved by cherry-picking or fabricating comparable sales, misrepresenting the property’s condition or square footage, ignoring adverse factors, or simply pressuring an appraiser to hit a predetermined number.

Detection combines valuation analytics with investigative scrutiny of the people involved. A forensic review re-examines the comparables actually available at the time, tests the adjustments the appraiser made, and flags valuations that are statistical outliers against contemporaneous market data. Investigators then look behind the number: undisclosed relationships between the appraiser, the loan officer, the buyer, and the seller; an appraiser whose files cluster suspiciously with one originator; and repeat participation in transactions that later defaulted. A single aggressive appraisal is a dispute. The same appraiser attached to a pattern of inflated values feeding a common set of beneficiaries is a scheme.

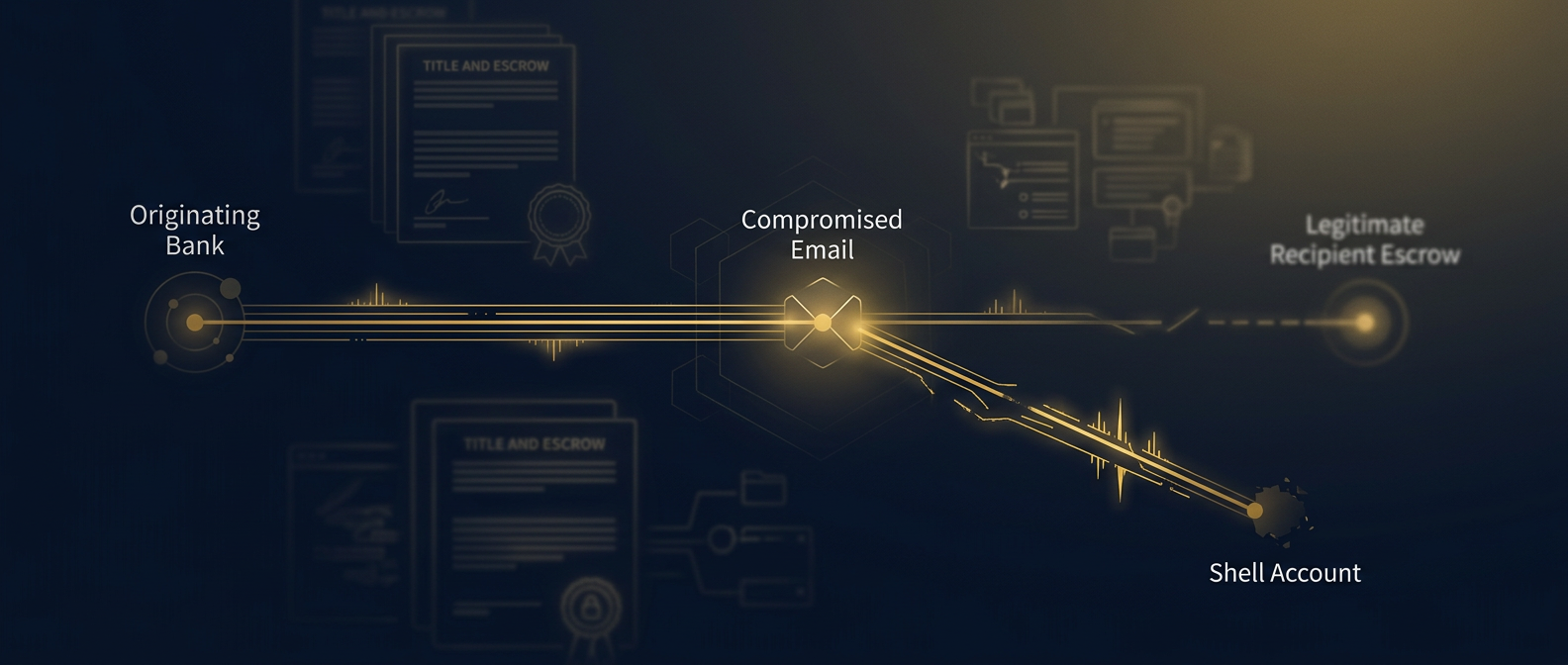

What makes closing wire fraud so dangerous?

Closing wire fraud is the fastest-moving and most financially devastating scheme in modern real estate, because it strikes at the moment the largest sum in the transaction is in motion. The mechanism is business email compromise: a fraudster monitors or spoofs the email of a title company, escrow officer, real estate agent, or lender, waits for a closing to approach, and sends the buyer — or the lender — last-minute “updated” wire instructions that route the funds to an account the fraudster controls. The money is withdrawn or moved through mule accounts within hours, often before anyone realizes the instructions were fraudulent.

Investigating wire fraud is a race against the clock and a forensic reconstruction after it. Speed governs recovery: an immediate report to the receiving bank and to the FBI’s Internet Crime Complaint Center (IC3), whose Recovery Asset Team can trigger financial-institution freezes, materially improves the odds of clawing funds back in the first 24 to 72 hours. The forensic side determines how the compromise occurred — which mailbox was breached, whether a look-alike domain was used, and what forwarding rules or credential theft enabled it — and preserves email headers, logs, and metadata as evidence. Attribution work then traces the destination account and its downstream movement to identify the beneficiaries and support both recovery litigation and criminal referral.

How are title and deed fraud investigated?

Title and deed fraud attacks ownership itself. Using a forged deed, a stolen or synthetic identity, and often a complicit or deceived notary, a fraudster purports to sell, mortgage, or transfer property they do not own. The favored targets are predictable: vacant land, absentee-owner and second-home properties, inherited homes in probate, and free-and-clear parcels held by elderly owners — assets where no one is watching the title day to day. The fraud may surface only when the true owner tries to sell, or when a lender forecloses on a loan the real owner never took.

The investigation rebuilds the chain of title and authenticates the instruments in it. Forensic document examination tests signatures, notary seals, and acknowledgment records for forgery; recording histories are reconstructed to locate the break where a fraudulent instrument entered the chain; and identity verification establishes whether the purported grantor was real, impersonated, or fabricated. Because deed fraud increasingly begins with identity theft and digital impersonation, the work frequently draws on the same forensic and background-intelligence disciplines used to unwind straw-buyer and synthetic-identity schemes.

How is occupancy and income misrepresentation proven?

Occupancy fraud — claiming a property will be owner-occupied to secure better terms while actually using it as an investment or rental — and income or asset misrepresentation are the most common fraud-for-housing schemes, and the most frequently underestimated. They matter because they distort the risk the lender priced, and because they are often the entry point that reveals a larger scheme.

Occupancy is proven or disproven through independent records that contradict the borrower’s declaration: utility usage, mailing and voter addresses, insurance designations, rental listings, and physical verification. Income and asset fraud is exposed through forensic analysis of the supporting documents — testing pay stubs, bank statements, and tax transcripts for alteration or fabrication, verifying employers and deposits against genuine sources, and reconciling stated income against lifestyle and cash flow. Fabricated employers, altered statements, and “gift” funds that are actually undisclosed loans are recurring findings. Here again, isolated misstatement differs from organized fraud: when the same fabricated employer or document template appears across multiple files, the case is no longer about one borrower.

What does a rigorous investigation actually involve?

A defensible mortgage-fraud investigation is disciplined, documented, and built for scrutiny by opposing counsel, an insurer’s claims committee, or a prosecutor. It is not a hunch confirmed after the fact; it is a repeatable process that produces attributable evidence. The following framework reflects how elite investigative teams structure the work:

- Scope and preserve. Define the suspected scheme and immediately preserve the evidence — the loan file, closing documents, email and system logs, and financial records — under sound chain-of-custody so nothing is altered or lost.

- Reconstruct the transaction. Build a complete timeline of the deal from application to funding, mapping every party, document, and dollar in the order they occurred.

- Authenticate the documents. Forensically examine appraisals, income and asset documents, deeds, and instructions for alteration, fabrication, forgery, and metadata inconsistencies.

- Trace the money. Follow the down payment, loan proceeds, and any diverted funds across accounts to establish true source, destination, and beneficiaries.

- Resolve the parties. Verify identities and expose hidden relationships and beneficial owners — straw arrangements, undisclosed conflicts, and the entities behind the names.

- Detect the pattern. Compare the transaction against others for recurring appraisers, closing agents, funding sources, LLCs, or addresses that reveal a coordinated scheme.

- Report for the decision at hand. Deliver a clear, evidence-backed findings report calibrated to its purpose — repurchase demand, insurance claim, civil recovery, or referral to law enforcement.

The through-line is evidentiary integrity. A finding that cannot survive challenge — because custody was broken, an assumption was untested, or a document was handled carelessly — is worse than no finding, because it can compromise recovery and referral alike.

How do investigators work with lenders, title firms, and counsel?

Mortgage fraud is rarely investigated in a vacuum; it is investigated in service of a decision that a lender, title insurer, or attorney has to make. The investigator’s job is to deliver intelligence that fits that decision and withstands the pressure it will face. For lenders and servicers, that means findings robust enough to support a repurchase demand, a buyback dispute, or a suspicious-activity referral. Financial institutions operate within a federal anti-money-laundering framework, and reporting obligations under the regime administered by the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN) increasingly reach real estate transactions and the professionals who facilitate them.

For title and escrow companies, the priority is speed and containment on wire fraud, plus authentication work that protects the insurer against a fraudulent claim on the policy. For general counsel and litigators, the investigation is frequently conducted under privilege, scoped to the elements the case must prove, and paired with expert testimony that presents forensic and financial findings credibly to a court. Across all of them, the constant is coordination: the investigator preserves and analyzes the evidence, and the client’s legal and compliance teams decide how to deploy it — recovery, litigation, insurance, or referral — on a foundation that holds.

How does Honeybadger investigate mortgage and real estate fraud?

Honeybadger Solutions investigates mortgage and real estate fraud as an integrated intelligence engagement, combining the disciplines these cases demand under one accountable team. Our investigations practice reconstructs the transaction, resolves straw arrangements and hidden beneficial owners, and traces the money through the accounts and entities that fraudsters use to launder it. Because our digital forensics, cybersecurity, financial-investigation, and background-intelligence capabilities are handled in-house, we can authenticate documents and appraisals, run email-header and business-email-compromise forensics on closing wire fraud, verify identities across borders, and preserve everything under defensible chain of custody — all without handing pieces of a sensitive matter to a chain of subcontractors.

Every engagement is scoped to the client’s objective, whether that is a lender’s repurchase or fraud-loss decision, a title insurer’s claim defense and wire-fraud recovery, or litigation and expert support for general counsel. As an Arizona-licensed firm serving lenders, title and escrow companies, law firms, and private principals nationwide and internationally, we bring the analytical rigor a financial institution expects and the discretion a private client requires. When funds have already moved, speed is decisive — and our teams are built to preserve evidence, trace destinations, and coordinate recovery from the first hours.

Frequently asked questions

What is the difference between a straw buyer and identity theft in a mortgage?

A straw buyer knowingly or unwittingly lends their real name and credit to obtain a loan for a hidden beneficiary, so the borrower on the file genuinely exists and applied. In identity-theft mortgages, the named borrower never applied at all — a stolen or synthetic identity was used without the real person’s knowledge. Both hide the true actor, but they are proven differently: the straw case turns on tracing funds and control to the beneficiary, the identity case on proving the named borrower had no involvement.

Can money lost to closing wire fraud be recovered?

Sometimes, and speed is the decisive factor. Funds diverted by a fraudulent wire are often moved out of the receiving account within hours, so recovery depends on immediate action — notifying the sending and receiving banks and filing with the FBI’s IC3, whose Recovery Asset Team can request financial-institution freezes. Reports made within the first 24 to 72 hours have materially better recovery odds. Forensic tracing of the destination account then supports civil recovery and criminal referral even when a full freeze is not achieved.

How do investigators prove an appraisal was fraudulent rather than just wrong?

By separating error from intent. A forensic review re-examines the comparable sales available at the time, tests the appraiser’s adjustments, and identifies valuations that are clear outliers against contemporaneous market data. Investigators then look for undisclosed relationships among the appraiser, originator, buyer, and seller, and for patterns — the same appraiser recurring across inflated, later-defaulting loans. A single aggressive valuation is a dispute; a documented pattern of manipulation feeding common beneficiaries is fraud.

Who should commission a mortgage fraud investigation?

Lenders and servicers facing suspicious defaults, repurchase disputes, or fraud losses; title and escrow companies responding to wire fraud or defending policy claims; general counsel and litigators building or defending a case; and private principals, investors, and family offices who suspect they were defrauded in a transaction. Any party relying on the integrity of a loan file, a title, or a set of closing funds has standing to have it independently examined.

About Honeybadger Solutions

Honeybadger Solutions is an Arizona-licensed security and investigations firm delivering mortgage and real estate fraud investigations, financial investigations, and cyber services to lenders, title and escrow companies, law firms, and private principals nationwide and internationally. Digital forensics, cybersecurity, financial investigations, and background intelligence are handled in-house; physical and executive protection is delivered through a commanded vetted-partner network directed from Arizona home command.

Offices: Casa Grande (HQ), Phoenix, and Oro Valley, Arizona — serving all Arizona, nationwide, and international clients.

Phone: 602-725-2818

Confidential consultation: discuss a suspected mortgage or real estate fraud matter with our investigations team.