When the subject of an investigation is a senior executive, the board—not management—must own it. Because that executive typically controls the company’s people, systems, counsel, and communications, the inquiry has to be structured for independence and secrecy from the first hour: an independent committee, independent outside counsel, an independent forensics vendor, covert evidence preservation, and a strict need-to-know circle. The stakes are not just employment; they are regulatory disclosure, market integrity, D&O coverage, and the reputation of the entire enterprise.

An investigation into a line employee is a self-contained problem. An investigation into a CEO, CFO, or founder is a governance crisis. The difference is power. The ordinary internal investigation assumes the organization can quietly point its own resources—HR, IT, in-house legal—at the subject. When the subject is the person those functions report to, every one of those resources is compromised the moment it is used. This is the discipline that separates a defensible board-level inquiry from one that collapses under later scrutiny, and it is unforgiving of shortcuts.

Why Is Investigating a Senior Executive Fundamentally Different?

Three features make executive misconduct a distinct category, and each one dictates a design choice in how the investigation is run.

- The subject controls the evidence. A senior executive commands the IT department that would normally image devices, the legal function that would normally supervise the inquiry, and the systems that hold the emails, messages, and financial records at issue. Using the company’s own IT to collect from the person IT answers to is not neutral collection—it is an invitation to tampering, tip-offs, and destroyed metadata.

- The subject controls the narrative. Executives control communications, investor relations, and often the board’s information diet. Left unchecked, a subject can frame the matter, discredit the reporter, or trigger a market-moving disclosure on their own terms before the board even understands the facts.

- The consequences are enterprise-level. Misconduct by an officer can implicate securities-disclosure duties, financial-statement integrity, insider-trading windows, directors’ and officers’ (D&O) insurance, lender covenants, and—if the conduct touches the books—the certifications executives sign under Sarbanes-Oxley. A finding against a warehouse supervisor rarely moves a share price; a finding against a CFO can.

Because of these features, the governing objective shifts from “find the facts” to “find the facts without the subject being able to distort, destroy, or front-run the process.” Independence and discretion are not niceties here; they are the load-bearing walls.

Who Should Own the Investigation—and Why Not Management?

The higher the subject sits, the further from them the investigation’s authority must originate. For most officer-level allegations, ownership belongs to the board, acting through its audit committee or a purpose-formed special committee of independent, disinterested directors. The committee’s independence is the single fact a regulator, plaintiff, or acquirer will test first. A committee that includes a director with a personal or business relationship to the subject is not independent, and its findings will be treated as such.

Independence has to run all the way down the chain:

- Independent directors charter and oversee the inquiry, insulated from the subject and from management who report to the subject.

- Independent outside counsel—not the company’s regular firm if that firm has a longstanding relationship with the subject—directs the investigation and holds the privilege.

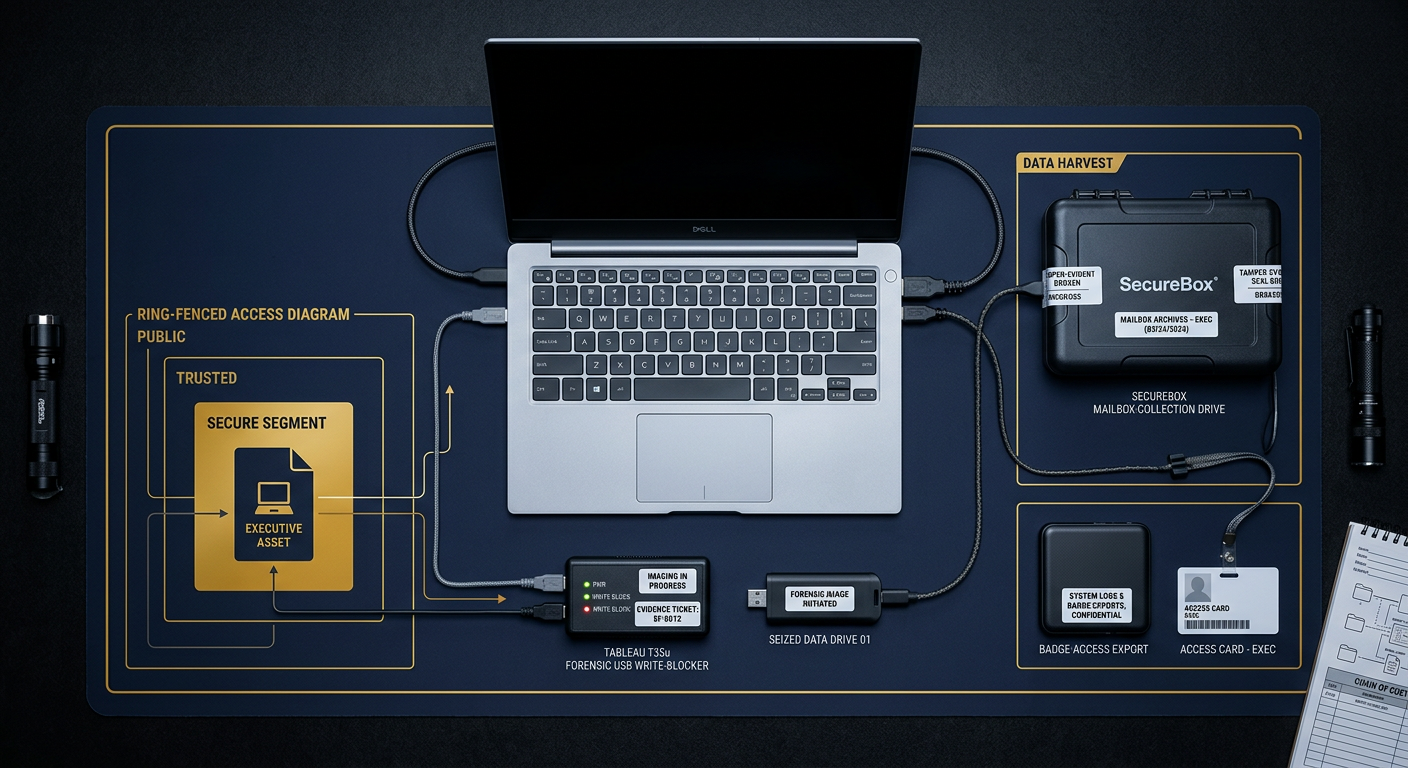

- An independent forensics and investigations vendor, retained by that counsel, collects and analyzes evidence. Company IT is deliberately excluded from collection touching the subject, because it cannot be neutral toward its own chain of command.

The pattern mirrors how the U.S. Department of Justice evaluates corporate self-investigation: prosecutors look for genuine independence and thoroughness, not a management-run exercise designed to reach a comfortable conclusion. The DOJ’s Evaluation of Corporate Compliance Programs makes clear that who conducts the inquiry, and how insulated they are, weighs heavily on whether the result is credited at all.

How Does an Executive Investigation Differ From a Standard One?

The workflow rhymes with any defensible internal investigation, but nearly every phase is hardened for independence and secrecy. The table below contrasts the two.

| Dimension | Standard internal investigation | Executive / C-suite investigation |

|---|---|---|

| Authority | HR or in-house legal opens it | Board audit or special committee charters it |

| Counsel | In-house or regular outside counsel | Independent outside counsel with no ties to the subject |

| Evidence collection | Company IT may assist | Independent forensics vendor; company IT ring-fenced out |

| Notice to subject | Often early once evidence is secured | Covert until preservation is complete; timing is a board decision |

| Information circle | Need-to-know within management | Need-to-know that may exclude the CEO/CFO entirely |

| External stakes | Employment, occasional litigation | Securities disclosure, D&O, lenders, market, headline risk |

| Endgame | Discipline, remediation | Possible resignation/clawback, disclosure, regulator contact, restatement |

The through-line is that authority and access are pulled up and out—away from the people who normally hold them—precisely because the normal holders answer to the subject.

How Do Boards Preserve Evidence Without Tipping Off the Executive?

Covert preservation is the most delicate operation in the entire matter. An executive who suspects an inquiry can delete messages, wipe devices, reroute email, alter records, or coordinate accounts of events—and unlike a junior employee, they often have administrative reach to do it quietly. The order of operations is therefore inverted from ordinary practice: preserve first, silently, and only then decide when the subject is told.

Done at an elite level, covert preservation relies on a few disciplines:

- Server-side collection before device-side. Where lawful and authorized, email and cloud data are preserved centrally—through legal-hold and eDiscovery mechanisms an independent vendor administers—so the record is captured without physically touching the executive’s laptop or phone and without a visible footprint on their machine.

- Ring-fenced administrative access. The subject’s ability to alter or purge relevant systems is quietly constrained, and any attempt to do so is logged. This is coordinated with a small, trusted group in IT security who do not report to the subject, or with an outside firm.

- Forensic imaging under authorization. Company-owned devices are imaged forensically—bit-for-bit, write-blocked, hashed—so that opening a file never alters the timestamps and deleted-file remnants that prove the case. Personal-device and privacy limits are mapped with counsel before anything is touched.

- A defensible chain of custody from item one. Every image, export, and log is acquired, hashed, sealed, and logged so it survives a courtroom challenge. Methodology tracks recognized forensic guidance such as that published by the National Institute of Standards and Technology.

This is the step where a board’s instinct to “just ask IT to pull his email” causes the most damage. The moment collection runs through a chain of command loyal to the subject, both the neutrality of the evidence and the secrecy of the inquiry are gone. Independent acquisition is the reason sophisticated boards route this work to an outside digital forensics team from the outset.

What Is the Discreet Executive-Investigation Protocol?

The following framework is the sequence an experienced board and its advisers follow. Each step exists to protect independence, secrecy, or defensibility—usually all three.

- Escalate to the independent directors. The credible allegation is routed away from management to the audit committee or lead independent director within hours, not days—bypassing any reporting line that runs through the subject.

- Charter the committee and confirm independence. A disinterested committee is formed or confirmed, and each member’s independence from the subject is documented. Conflicted directors recuse.

- Retain independent counsel. The committee engages outside counsel with no material ties to the subject or management, in a written engagement that establishes legal purpose and privilege.

- Retain an independent forensics and investigations firm. Counsel engages the investigative vendor as its agent, extending privilege over the technical work and keeping collection out of company IT’s hands.

- Preserve covertly. Evidence is captured server-side and forensically before the subject is aware, with administrative reach ring-fenced and every action logged.

- Draw the need-to-know circle tight. A written list defines who knows—often excluding the CEO/CFO and most of management. Everyone in the circle is instructed on confidentiality and the consequences of a leak.

- Build the record before interviews. Forensic and financial analysis reconstructs the timeline from data, not memory, so any eventual interview tests the subject’s account against evidence already in hand.

- Assess disclosure and market obligations in parallel. Securities counsel evaluates, on an ongoing basis, whether the facts trigger a duty to disclose, a trading blackout, or a filing—before, not after, the investigation concludes.

- Interview the subject last, on the committee’s timing. The executive is confronted only once preservation is complete and the documentary picture is built, with an Upjohn-style warning that counsel represents the company, not the individual.

- Report to the board and act. Findings go to the independent committee in the format counsel specifies, driving decisions on separation, clawback, disclosure, regulator contact, and control remediation.

How Is Privilege Protected at the Board Level?

Privilege in an executive investigation is both more valuable and more fragile than usual, because the eventual audience may include the SEC, the DOJ, plaintiffs’ counsel, an acquirer’s diligence team, and the subject’s own lawyers. Two principles govern.

First, privilege attaches only when the inquiry is conducted at the direction of counsel for the purpose of legal advice. That is why the committee retains counsel, and counsel retains the forensics firm as its agent—so the technical work product falls within the privilege rather than outside it. Second, the company, not the executive, holds and controls that privilege. Every interview a subject or witness gives should open with the warning that company counsel does not represent them individually and that the company alone decides whether to waive. Skipping that warning is a classic way privilege unravels one conversation at a time.

A distinct board-level tension is the possibility of a selective waiver—voluntarily sharing findings with a regulator to earn cooperation credit while trying to preserve privilege against private plaintiffs. Courts treat this inconsistently, so the decision is made deliberately by counsel with the full downstream picture in view, never as an offhand gesture of goodwill.

What Are the Regulatory and Reputational Stakes?

This is where an executive investigation stops being an HR matter and becomes an enterprise-risk event. The board’s advisers track several exposures at once:

- Securities disclosure. For public companies, misconduct by an officer—especially anything touching financial reporting—can create a duty to disclose and, in serious cases, a Form 8-K trigger. The U.S. Securities and Exchange Commission expects timely, accurate disclosure and scrutinizes internal-control failures behind executive fraud.

- Insider-trading exposure. The pendency of a material internal investigation is often itself material non-public information. Trading windows may need to close for insiders while the matter is live.

- D&O insurance. Timely, correct notice to the D&O carrier preserves coverage; late or mishandled notice can forfeit it. Fraud findings may also void coverage for the individual.

- Clawbacks and certifications. Sarbanes-Oxley and exchange clawback rules can require recovery of incentive compensation from officers where misconduct drove a restatement.

- Reputation and market confidence. A leak, a botched disclosure, or a perceived cover-up can do more lasting damage than the underlying conduct. The way the board is seen to have handled the matter becomes part of the story.

Private companies face a narrower but real version of the same map: lender covenants, investor-rights agreements, insurance notice, and the trust of the founders and funds around the table.

How Do You Keep the Investigation From Leaking?

Discretion is a discipline, not a hope. Leaks in executive matters come from predictable places—an over-wide notification, a careless calendar invite, a document left on a shared drive, a rushed vendor onboarding—and each is preventable.

- Minimize the circle by design. Fewer people means fewer failure points. The need-to-know list is written, justified, and revisited—not allowed to sprawl.

- Keep work product off company infrastructure. Independent counsel and the forensics firm work in their own secured environments, not on systems the subject or their allies can reach.

- Control the paper trail. Codenames for the matter, restricted document repositories, and disciplined version control keep the inquiry from surfacing in ordinary company systems.

- Prepare communications before they are needed. Holding statements for employees, investors, and—if necessary—the press are drafted in advance with counsel, so a forced disclosure is met with a considered message rather than improvisation.

- Coordinate any surveillance or field work centrally. Where an executive matter extends to physical activity—asset verification, undisclosed conflicts, or protective concerns—those elements are commanded discreetly and lawfully through vetted specialists, not local improvisation.

The financial dimension—self-dealing, undisclosed related-party transactions, expense abuse, or manipulated results—almost always runs alongside the conduct question and is traced through our financial investigation practice, while conflict-of-interest and undisclosed-relationship questions draw on corporate investigations and discreet background intelligence.

National Reach, Boardroom Discretion

Honeybadger Solutions supports boards, audit committees, and their independent counsel on sensitive executive matters across Arizona, nationwide, and internationally. Our digital forensics, cybersecurity, financial investigations, and background intelligence capabilities are in-house and remote-by-design, so an independent committee can stand up covert preservation and analysis within hours—regardless of where the executive or the evidence sits—without ever routing collection through the company’s own IT chain. Where a matter extends into physical or protective operations, we command a vetted-partner network with Arizona as home command and established theaters in California, Texas, and Florida. We serve as counsel’s independent investigative arm, and the record we build is designed to withstand a regulator, an acquirer, and a courtroom. Explore our corporate investigations and security capabilities, or reach our teams through the Phoenix office.

Frequently Asked Questions

Why can’t management investigate its own executives? Because HR, in-house legal, and IT all report through the chain of command the subject controls, they cannot be neutral toward that person and cannot keep the inquiry secret from them. For officer-level allegations, the board acting through an independent or special committee owns the investigation, engages independent outside counsel, and retains an independent forensics vendor so that authority and evidence collection sit outside the subject’s reach.

How do you investigate an executive without them finding out? Preservation runs first and silently: email and cloud data are captured server-side through legal-hold and eDiscovery tools an independent vendor administers, company-owned devices are imaged forensically under authorization, and the subject’s ability to alter systems is quietly ring-fenced and logged. The subject is interviewed only after the documentary record is built and preservation is complete, on the committee’s timing.

When does an executive investigation have to be disclosed? There is no single trigger, but for public companies a material internal investigation—particularly one touching financial reporting or an officer’s integrity—can create disclosure duties, an 8-K obligation, and a need to close insider trading windows. Securities counsel assesses disclosure and D&O-notice obligations continuously, in parallel with the fact-finding, not only at the end.

How is attorney-client privilege protected in a board investigation? The independent committee retains outside counsel, and counsel retains the forensics and investigations firm as its agent, so the technical work is done for the purpose of legal advice and falls within the privilege. The company—not the executive—controls that privilege, every interview opens with an Upjohn-style warning, and any decision to share findings with a regulator is made deliberately by counsel because selective waiver is treated inconsistently by courts.

About Honeybadger Solutions

Honeybadger Solutions is an Arizona-licensed security and investigations firm serving all of Arizona, the nation, and international clients. We combine in-house digital forensics, cybersecurity, financial investigations, and background intelligence with a vetted network for field and protective operations. We work as the independent investigative arm of boards, audit committees, and their outside counsel on sensitive executive matters—building discreet, defensible records that withstand regulatory, litigation, and transactional scrutiny.

Three offices: Casa Grande (HQ), Phoenix, and Oro Valley. To discuss a confidential matter, call 602-725-2818. Learn more about our corporate and internal investigations capabilities and request a discreet, privileged consultation.