Hidden income for child support is proven by pairing lawful family-court discovery — sworn financial affidavits, subpoenas, and depositions — with forensic accounting and lifestyle analysis that measure a parent’s true earnings against what they declared. Investigators trace unreported cash, off-books and 1099 work, business perks run as personal spending, and deferred or manipulated pay, then assemble court-admissible documentation so guideline support reflects real earning capacity rather than a manufactured shortfall.

Child support is one of the few financial obligations a court sets almost entirely on a single number: the income of the parents. That makes income the battlefield. A parent who wants to pay less has one dominant strategy — make their earnings look smaller than they are — and the family-court forum, which relies heavily on self-reported financial affidavits, gives them room to try. This guide is written for the family-law attorney, custodial parent, guardian, and financially sophisticated principal who needs to understand how income is actually concealed, why child-support cases turn on a different set of facts than asset-division cases, and how a disciplined, lawful investigation reconstructs a parent’s true earning power to a standard a judge will accept. The goal is not punishment; it is an accurate income figure on which a child’s support is honestly calculated.

Why is hidden income different from hidden assets?

In a divorce, the fight is often over a static pool of property to be divided once. Child support is different: it is a recurring, forward-looking obligation driven by income and earning capacity, and it can be revisited for years as circumstances change. A hidden bank account matters in a support case mainly for what it reveals about the income flowing into it. That shift in focus changes the entire investigative posture — the question is not “what does this parent own?” but “what does this parent actually earn, and what could they earn if they were not deliberately suppressing it?”

Two features make support cases uniquely prone to income games. First, nearly every U.S. jurisdiction runs support through a guideline formula — most states use an Income Shares model, a minority a Percentage of Income model — where each additional dollar of proven income raises the obligation in a predictable way, giving the paying parent a sharp incentive to hide the marginal dollar. Second, the definition of “income” for support is deliberately broad and often includes items a parent does not think of as pay: perks, in-kind benefits, recurring gifts, and, critically, potential income the court can impute to someone who is voluntarily underemployed. A world-class investigation exploits both features — it finds the concealed real income and it builds the record to impute income the parent is choosing not to earn.

How do parents actually hide or understate income?

Understanding the playbook is the foundation of dismantling it. Income concealment clusters into a handful of recognizable patterns, each with characteristic tells and a corresponding investigative counter. The table below maps the most common tactics, how they work, and how a lawful investigation surfaces each one.

| Concealment tactic | How it works | How investigators surface it | Difficulty |

|---|---|---|---|

| Unreported cash income | Skimming from a cash-intensive business, tips, side jobs, and “under-the-table” pay never deposited or reported | Lifestyle analysis, bank-deposit reconstruction, comparison of declared income to spending, industry-norm benchmarking | High – leaves indirect traces |

| Off-books & 1099 / gig work | Contract, freelance, gig-platform, or 1099 income omitted from the affidavit or paid to a friend’s account | 1099 and platform records, payment-app and merchant-processor subpoenas, client and vendor confirmation, tax-transcript review | Medium |

| Business income manipulation | Loading a closely held company with personal expenses, phantom payroll, and owner “loans” to depress take-home pay | Forensic accounting of the ledger, add-back analysis of personal perks, tax-return-to-books reconciliation | High – needs accounting expertise |

| Deferred & timed compensation | Delaying bonuses, commissions, distributions, or a raise until after support is set; quitting or “reducing hours” strategically | Employer records, historical earnings pattern, deposition testimony, timing analysis around the filing date | Medium |

| In-kind & third-party support | Employer or family paying housing, vehicle, phone, or living costs so the parent needs little on-paper income | Perquisite tracing, lifestyle documentation, review of who actually pays recurring bills | Medium |

| Voluntary underemployment | Taking a lower-paying role, going “unemployed,” or working below qualifications to shrink the guideline number | Vocational evidence, work and licensing history, labor-market data to support imputation of income | Medium–High |

Two patterns fall out of that map. First, the most durable concealment almost always runs through self-employment or a closely held business, because that is where a parent controls both the reported number and the plausible cover for moving money. A W-2 wage earner with a single employer has little room to maneuver; a contractor, small-business owner, or gig worker has many levers. Second, nearly every tactic eventually collides with a record a third party keeps — a bank, a payment processor, a gig platform, a tax authority, or a lender — and it is those independent records, lawfully obtained, that break a concealment case open.

What counts as income for child support?

Half of these cases are won not by finding hidden money but by correctly characterizing money that is hiding in plain sight. Support guidelines define income expansively. Beyond salary and wages, courts routinely count self-employment net income, bonuses and commissions, overtime, tips, investment and rental income, retirement and disability payments, and, in many jurisdictions, recurring gifts and in-kind benefits that reduce personal living expenses — a company car, employer-paid housing, or a family member consistently covering the rent. The federal framework administered by the Office of Child Support Services leaves the precise definitions to each state, but the theme is consistent: the guideline is meant to capture a parent’s real economic ability to support a child, not a narrow paycheck figure.

This is why the single most valuable document in a support case is often the tax return — and, more precisely, the official tax transcript obtained directly from the Internal Revenue Service rather than a copy the parent hands over. A transcript shows W-2 and 1099 income reported to the government, Schedule C business results, interest and dividends that reveal unlisted accounts, and capital gains that imply investable wealth. When a parent’s return reports figures that cannot support the life the family actually lived, the contradiction is documented in the parent’s own sworn filing. Loan and credit applications are the mirror image: a parent understating income to the support court has frequently overstated that same income to a lender months earlier, and reconciling the two sworn numbers is often where the case is decided.

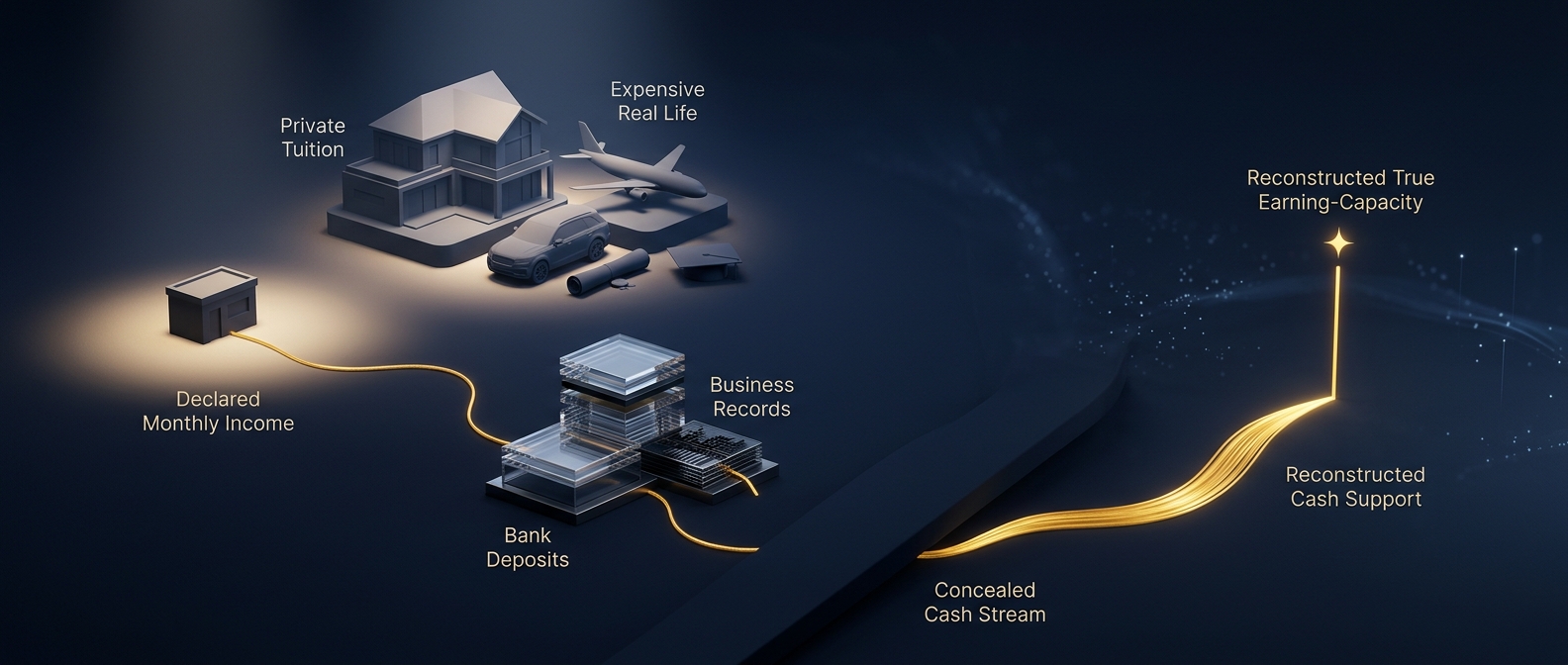

How does lifestyle analysis expose understated income?

Lifestyle analysis is the workhorse of a hidden-income investigation, because it turns an abstract suspicion into a quantified, defensible number. The technique is straightforward in principle and rigorous in execution: build a detailed picture of how a parent actually lives — housing, vehicles, travel, private tuition, dining, hobbies, recurring subscriptions, and discretionary spending — and compare that documented cost of living against the income they claim. When someone reports $40,000 a year but services a lifestyle that plainly costs three times that, the shortfall has to be funded from somewhere, and that somewhere is almost always unreported income.

Executed at an elite level, this is a bank-deposit and cash-flow reconstruction rather than an impression. Investigators total the deposits into every known account, identify sources for each, and flag deposits and cash purchases that no declared income stream can explain. They document who pays the recurring bills, whether a business is absorbing personal costs, and how spending compares to industry norms for the parent’s trade. The output is not “this parent seems to be doing well” but a source-backed statement that the parent’s spending and deposits require an income of a specific magnitude — the same investigative rigor our investigations and financial-investigation teams apply to fraud and asset-recovery matters, here focused on establishing true earning power for a child’s benefit.

What lawful methods build admissible income evidence?

Everything a legitimate investigation produces must be obtained lawfully and be admissible in family court — hidden income proven through an unlawful method is worse than useless, because it can taint the case and expose the client to liability. The engine of disclosure is the formal discovery process, driven by counsel and supported by the investigative team. The core instruments are the sworn financial affidavit each parent must file; interrogatories and requests for production compelling tax returns, pay records, bank and payment-app statements, and business books; subpoenas to employers, banks, gig platforms, and merchant processors that hold records directly; and depositions that lock a parent into sworn testimony an investigator can then test against the paper trail.

Independent open-source and public-records work runs alongside discovery, always within the law. Business filings and licensing records confirm ownership and active operation; court and UCC records reveal financing that implies income; and lawful, non-intrusive documentation of a parent’s outward business activity — advertised services, active job sites, or a storefront doing steady trade — can corroborate cash volume that never appears on a return. Where digital records are in play, our digital forensics capability can lawfully examine devices and accounts the client controls to recover invoices, payment-app histories, and client communications that establish off-books work. The discipline that ties it together is authentication: every figure is anchored to a source record with a documented chain of custody, so it survives cross-examination rather than collapsing under it.

What is the step-by-step process for a hidden-income investigation?

A world-class hidden-income investigation follows a disciplined sequence, run in coordination with family-law counsel so that every finding is both lawful and usable. The order matters: baseline and preservation first, targeted tracing second, a defensible income figure last.

- Preserve and baseline. Secure the records and any devices the client lawfully controls before anything is deleted, and assemble the known picture — tax transcripts, pay and 1099 records, bank statements, the sworn affidavit, and prior loan applications.

- Characterize the income correctly. Map every stream against the jurisdiction’s broad support definition — wages, self-employment, perks, in-kind support, and recurring gifts — so nothing legitimate is missed before hunting for what is hidden.

- Run the lifestyle analysis. Document how the parent actually lives and reconstruct deposits and cash flow to quantify the gap between declared income and the income the lifestyle requires.

- Trace off-books and 1099 work. Pursue gig-platform, payment-app, and merchant-processor records; confirm clients and vendors; and identify contract income routed around the parent’s own accounts.

- Examine the business. Where a closely held company exists, analyze the ledger for personal expenses run through the entity, phantom payroll, and owner distributions, and add back perks that are really compensation.

- Build the imputation record. Where the parent is voluntarily underemployed, gather work history, credentials, and labor-market evidence supporting the income a court can attribute to their true earning capacity.

- Compel third-party records. Support counsel in subpoenaing employers, banks, platforms, and processors, and in deposing the parent and relevant third parties.

- Deliver court-ready evidence. Produce a clear report, authenticated exhibits, and, where needed, expert testimony that states the true income figure and withstands challenge.

Each step narrows the question from “is this parent hiding income?” to “exactly how much, from what sources, documented how” — the specificity that moves a judge and sets support correctly.

When can a court impute income to an underemployed parent?

Some parents do not hide income so much as decline to earn it. Anticipating this, guideline systems in most states allow a court to impute income — to calculate support based on what a parent could earn — when the court finds the parent is voluntarily unemployed or underemployed without a legitimate reason. A high earner who abruptly “retires,” a licensed professional who takes minimum-wage work, or a business owner who conveniently reports near-zero profit can all be candidates for imputation. This turns a suppression strategy into a liability, because the court can look past the manufactured number to the parent’s real earning capacity.

Building an imputation case is evidentiary work. It combines the parent’s documented work history, education, licenses, and prior earnings with objective labor-market data — the kind of wage and occupational information published by the U.S. Bureau of Labor Statistics through its Occupational Employment and Wage Statistics program — to establish what someone with that profile earns in the relevant market. In contested matters a vocational assessment strengthens the record. The result is a defensible earning-capacity figure the court can adopt, so a parent cannot escape a fair obligation simply by choosing to earn less than they are able.

What separates a world-class investigation from a mediocre one?

The difference is rarely effort; it is discipline, integration, and admissibility. A mediocre effort produces a folder of screenshots and a hunch. A world-class one produces a quantified, source-backed statement of the parent’s true income that a judge can rely on and opposing counsel cannot dismantle. The decisive factors are whether the financial investigation, digital forensics, and open-source intelligence live under one accountable roof rather than being farmed out to disconnected vendors; whether every figure is tied to an authenticated record with a documented chain of custody; and whether the team understands the support forum well enough to build evidence that is not merely persuasive but provable and lawfully obtained.

Cost tracks complexity, and candor about the drivers helps set expectations: whether self-employment or a business is involved, the number of income streams and accounts, the presence of cash or gig income, whether imputation and a vocational component are needed, and how hard the other side fights discovery. A straightforward W-2 dispute may need only targeted record analysis; a self-employed parent with cash income, a padded business, and voluntary underemployment warrants a full forensic engagement — and because support is a multi-year obligation, an accurate figure compounds in value over the life of the order. The unifying principle at every budget is the same: never trade method for speed, because an inadmissible finding is not a finding at all.

How does Honeybadger approach hidden-income matters?

Honeybadger Solutions approaches child-support income investigations the way they must be run to hold up in court: lawfully, in coordination with the client’s family-law counsel, and to a defensible evidentiary standard. Because our financial investigations, digital forensics, cybersecurity, and background-intelligence capabilities are handled in-house and delivered nationwide and internationally, a hidden-income matter never fragments across mismatched vendors. The same command that reconstructs the flow of funds also examines the devices, traces the off-books and gig income, characterizes the business perks, and packages the exhibits and expert support that counsel needs at deposition and hearing.

Our investigations practice serves parents, guardians, family offices, and matrimonial attorneys across the United States and abroad, drawing on the same discipline we apply to fraud, asset recovery, and diligence work. From Arizona home command — with offices in Casa Grande, Phoenix, and Oro Valley — we bring a parent’s true earning power into focus so support is calculated on the truth rather than on an edited version of it. Every scenario described here is representative; every engagement is confidential, method-first, and built to survive challenge for the benefit of the child.

Frequently asked questions

Can you really prove a parent is hiding cash income?

Yes, though cash requires indirect proof. Investigators use lifestyle analysis and bank-deposit reconstruction to show that a parent’s documented spending and deposits require far more income than they declared, then anchor the gap to source records — tax transcripts, payment-app and processor histories, business books, and third-party bills. Courts routinely accept a well-documented reconstruction that demonstrates a specific unexplained income magnitude, especially in cash-intensive trades where the declared figure defies industry norms and the observed lifestyle.

What is imputed income and when does it apply?

Imputed income is earnings a court attributes to a parent based on what they could earn, used when a judge finds the parent voluntarily unemployed or underemployed without good reason. It applies to a high earner who abruptly stops working, a professional taking work far below their qualifications, or an owner reporting implausibly low profit. The case is built from work history, education, licenses, prior earnings, and labor-market wage data, sometimes supported by a vocational assessment. Standards vary by state, so confirm specifics with counsel.

Is it legal to investigate the other parent’s income?

Investigating income is legal when done through lawful means — the formal discovery process, subpoenas to third parties, public-records and open-source research, and forensic analysis of records and devices you lawfully control. What is not legal is accessing the other parent’s accounts without authorization, intercepting communications, or installing spyware; such conduct can expose you to liability and render evidence inadmissible. This is why a hidden-income investigation should always run in coordination with your family-law attorney and within statutory limits.

What documents matter most in a child-support income case?

The official IRS tax transcript, W-2 and 1099 records, complete bank and payment-app statements, business ledgers and returns, and any recent loan or credit applications carry the most weight. Tax transcripts show income reported to the government; loan applications often reveal income the parent later understated to the court; and bank and platform records expose deposits and gig work missing from the affidavit. Authenticated third-party records almost always outweigh a parent’s self-reported financial affidavit.

About Honeybadger Solutions

Honeybadger Solutions is an Arizona-licensed security and investigations firm delivering intelligence-led financial investigations, forensics, and cyber services to parents, guardians, general counsel, and matrimonial attorneys nationwide and internationally. Financial investigations, digital forensics, cybersecurity, and background intelligence are handled in-house, so a hidden-income matter is preserved, traced, and reconstructed under a single accountable chain of command — lawfully, in coordination with your family-law counsel, and to a court-admissible standard.

Offices: Casa Grande (HQ), Phoenix, and Oro Valley, Arizona.

Phone: 602-725-2818

Confidential consultation: discuss a suspected income concealment with our command team and your family-law attorney — the earlier records are preserved, the more can be proven.